- February 22, 2024

- Posted by: Shane Daly

- Categories: Options Trading, Trading Article

Imagine you’ve purchased a call option with a premium of $200, banking on the stock of XYZ Corporation to rise before expiration. As each day passes, you notice the value slowly shrinking, even though the stock price hasn’t moved against you. This invisible force at work is theta decay or time decay, an important part of the options pricing model that eats away at an option’s value as it approaches its expiration date.

Imagine you’ve purchased a call option with a premium of $200, banking on the stock of XYZ Corporation to rise before expiration. As each day passes, you notice the value slowly shrinking, even though the stock price hasn’t moved against you. This invisible force at work is theta decay or time decay, an important part of the options pricing model that eats away at an option’s value as it approaches its expiration date.

While the concept might seem straightforward, the variables that contribute to the rate of decay—such as volatility and the time remaining until expiration—interact in complex ways in the way options are priced.

Key Takeaways

- Theta decay is the erosion of an option’s value as the expiration date approaches, and it directly impacts potential profits in options trading.

- Monitoring volatility and expiry proximity is crucial for adapting strategies to theta decay, as higher volatility and closer expiration dates accelerate the decay process.

- Theta decay can be calculated using the theta value, which quantifies the expected decline in an option’s premium as expiration approaches.

- Mitigating theta decay can be achieved through strategies such as diversifying portfolios, incorporating calendar spreads, and utilizing short-term options for rapid adjustments in fast-moving markets.

Understanding Theta Decay

Theta decay, also known as time decay, is a fundamental concept in options trading, representing the erosion of an option’s value as the expiration date approaches. This directly influences the profitability of options positions and plays an important role in shaping the trading strategies you will use.

Imagine theta decay as the ticking clock within the options market, eating away at the value of option contracts as time progresses. This erosion occurs regardless of whether the underlying asset’s price moves favorably or unfavorably for the option holder.

Imagine theta decay as the ticking clock within the options market, eating away at the value of option contracts as time progresses. This erosion occurs regardless of whether the underlying asset’s price moves favorably or unfavorably for the option holder.

Even if the market remains in a trading range, the option’s value will gradually decline over time due to theta decay.

Consider a scenario where you purchase a call option on a stock with an expiration date several months away. Initially, the option’s premium may be relatively high, reflecting the potential for price movements in the underlying asset.

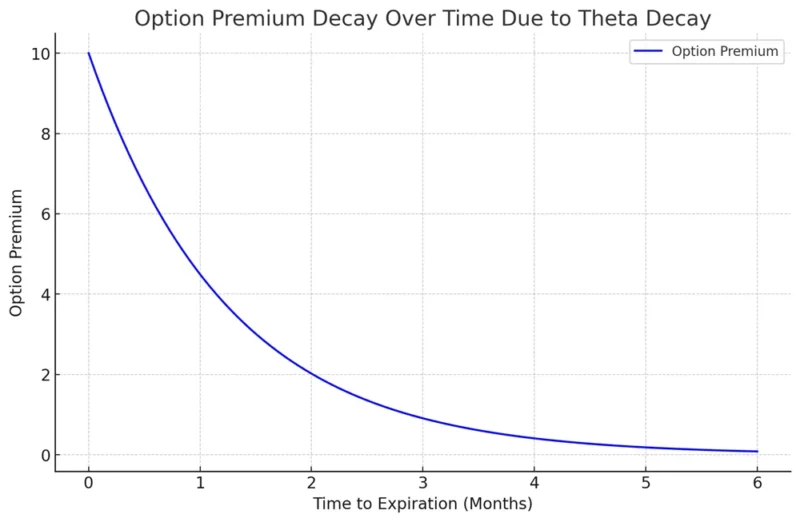

As time elapses and expiration draws nearer, the theta decay accelerates, causing the option’s premium to decline steadily. If the underlying stock fails to move sufficiently in your favor before expiration, the impact of theta decay can significantly erase your potential profits.

Theta and Option Premiums

As the expiration date of an option draws closer, the premium you’ve paid shrinks. This time decay accelerates as expiration dates get closer, steadily eroding the value of your option. Understand that theta isn’t a one-size-fits-all measurement; it varies across different options and market conditions.

Remember that options with more time until expiration are less sensitive to theta decay. Conversely, short-term options can lose value rapidly, making timing your entry and exit strategies that much more important.

Factors Affecting Theta

Recognize that volatility influence plays a significant role. High market volatility can lead to larger option premiums, which in turn affects theta decay. The reason is simple: the more volatile an asset, the greater the chance of significant price swings, which boosts the value of the time remaining on an option.

Expiry proximity is another critical factor. As the expiration date of your option draws closer, theta decay tends to accelerate. This means that the option loses value at an increasing rate as time runs out.

Calculating Theta Impact

Understanding how theta values are determined and how they vary across different options and market conditions is essential for effectively managing options positions.

Understanding Theta Value

Theta values are derived from complex mathematical models used to price options, such as the Black-Scholes model or its variants. These models take into account various factors, including the time to expiration, the volatility of the underlying asset, the risk-free interest rate, and the option’s strike price.

Theta values are typically expressed as negative numbers, reflecting the decrease in an option’s premium as time passes. The magnitude (how large the price change will be) of theta depends on several factors, including:

Theta values are typically expressed as negative numbers, reflecting the decrease in an option’s premium as time passes. The magnitude (how large the price change will be) of theta depends on several factors, including:

- Time to Expiration: Theta tends to increase as the expiration date approaches, reflecting the accelerating rate of time decay. Options with shorter time to expiration generally have higher theta values than those with longer timeframes.

- Volatility: Higher levels of volatility in the underlying asset tend to result in higher option premiums, leading to larger theta values. This is because increased volatility implies a greater likelihood of significant price movements, which contributes to the time value of the option.

- Strike Price: Theta values may vary depending on the proximity of the option’s strike price to the current market price of the underlying asset. At-the-money options typically have higher theta values than out-of-the-money or in-the-money options.

Example Theta Calculations

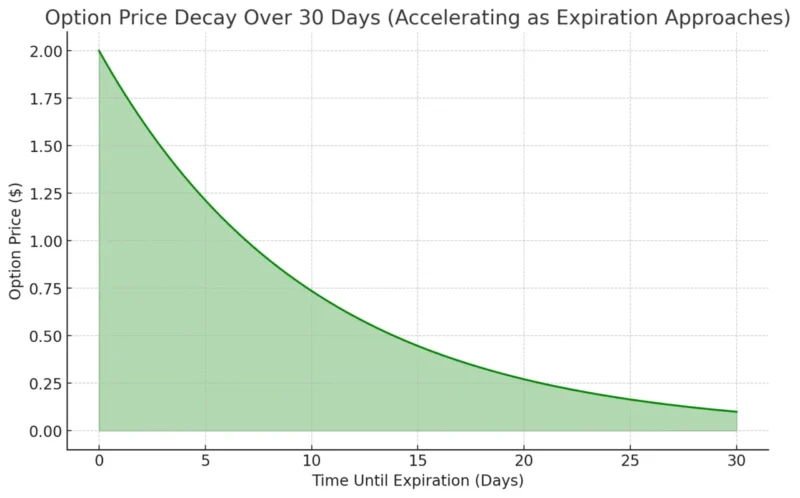

Suppose you purchase a call option on a stock with a theta value of -0.05. This means that the option’s premium is expected to decrease by $0.05 for every day that passes. If there are only 7 days remaining until expiration, the total theta decay over the next week would not be a simple calculation of -0.05 x 7 = -$0.35 as it does not take into account the faster acceleration of theta decay as expiration approaches.

Theta is not a linear measure, and the rate of theta decay increases as the time remaining until expiration decreases. In the final week or days leading up to expiration, theta decay becomes more significant. As a result, the premium can decline at a faster pace than the daily rate would initially suggest.

To accurately account for this, we can estimate the faster acceleration of theta decay by incorporating a higher daily decay rate. Let’s assume that the accelerating effect of theta on the option premium leads to an estimated average daily decay rate of $0.10 in the final week. The total theta decay over the next 7 days would be:

Total Theta Decay = Theta Value = -0.10 x 7 = -$0.70

In this case, with only 7 days left until expiration, the option’s premium would decrease by an estimated $0.70 over the next week due to the faster acceleration of theta decay.

This adjustment accounts for the increasing rate at which the option’s premium declines as expiration approaches, reflecting the impact of the accelerating effect of theta.

Theta’s Daily Decay Rate

Here’s what you need to know:

- Time Sensitivity: Options lose value as expiration nears, with decay-accelerating in the final weeks.

- Strategic Adjustments: Adapt your strategies to account for decay patterns; sell options to capitalize on theta.

- Daily Calculation: Estimate daily decay by dividing theta by the number of days left.

Your success in trading hinges on understanding this.

Mitigating Theta’s Effects

Understanding how to counteract theta’s effect on premiums is something you should know. Choosing short-term contracts can minimize the impact, as they’re less susceptible to time decay.

Meanwhile, diversifying your strategies and incorporating calendar spreads offer additional layers of defense against the relentless tick of the theta clock.

Choose Short-Term Contracts

To mitigate the impact of theta decay on option premiums, consider selecting short-term contracts where the time erosion of value is less pronounced. It’s about striking the right balance between expiration proximity and contract selection to maximize your gains while keeping the decay at bay.

Here’s how you can harness the power of short-term options:

- Rapid Adjustments: Short-term contracts allow you to pivot quickly in fast-moving markets, giving you the ability to capitalize on sudden movements.

- Lower Premiums: They typically come with lower premiums, freeing up capital for other investments or strategies.

- Sharper Responses: With shorter durations, you’re more attuned to market signals, enabling decisive action that aligns with your quest for financial freedom.

Embrace short-term options and let your strategy be as dynamic as the markets themselves.

Using Diversified Options Strategies

Diversifying your options strategies can effectively counteract the erosive effects of theta decay, ensuring that your portfolio isn’t overly exposed to the risks associated with time-sensitive securities. Think of it as a form of risk assessment that’s continually in motion, adapting to market changes.

- Strategically combine long and short positions

- Explore a mix of expiration dates

- Consider using various strike prices.

This way you are not on the defense with Theta but being proactive in managing its effects on Options.

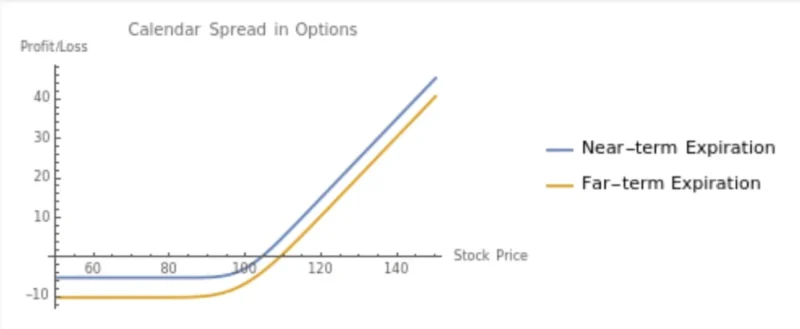

Use Calendar Spreads

Consider using calendar spreads to mitigate the impact of theta decay on your options portfolio. Calendar strategies offer an approach to managing time decay, turning it from an adversary into an ally. By entering a spread that involves different expiration dates, you create an opportunity to profit from the varying rates of theta decay.

Consider using calendar spreads to mitigate the impact of theta decay on your options portfolio. Calendar strategies offer an approach to managing time decay, turning it from an adversary into an ally. By entering a spread that involves different expiration dates, you create an opportunity to profit from the varying rates of theta decay.

Here’s how you can leverage calendar spreads:

- Capitalize on Different Decay Rates: Sell a short-term option to benefit from faster decay, while holding a longer-term option with a slower decay rate.

- Make Timely Spread Adjustments: Actively manage your positions to respond to market movements and volatility shifts.

- Take Profits: Close out or roll positions to capture value at optimal moments, enhancing your financial freedom.

This will take practice and trial and error but eventually, you will have a robust approach to tackling Theta issues with your trades.

Timing Trades With Theta

Understanding how theta decay impacts option premiums can significantly improve your timing when entering or exiting trades. With the right option strategies, you’re not just predicting market movements; you’re also leveraging time to work in your favor.

As market volatility shakes up the prices, theta decay chips away at the value of options as expiration approaches.

Here’s a plan to consider:

- Use strategies that capitalize on accelerated theta decay.

- Think about selling options when theta’s impact is most potent—typically closer to expiration.

- If you’re buying, do it when you can minimize the cost of time decay.

Summary

Mastering the concept of theta decay is important to find consistent success with trading options. With each passing day, theta eats away at option premiums, affecting the profitability of your positions.

Reflect on how you can use this knowledge in your trading strategies. Are there adjustments you can make to mitigate the effects of time decay on your options portfolio? Are there new strategies you can explore to capitalize on theta decay?

FAQ

How does theta affect the price of an option?

Theta is a measure of the rate of decline in the value of an option due to the passage of time. It can also be referred to as the time decay of the option. This means if all other factors remain constant, an option will lose value as time draws closer to its maturity. Theta has a negative impact on the price of an option.

How does time decay affect the price of an option?

Time decay is a measure of the rate at which an option loses value over time. As an option approaches its expiration date, the probability of it being profitable decreases, which in turn decreases its value. This is why options are considered wasting assets; they lose value over time if all other factors remain constant.

What is the factor affecting option premium?

Several factors affect the premium of an option including the underlying asset price, the strike price of the option, the time until expiration, the volatility of the underlying asset, and the risk-free interest rate. Among these, the price of the underlying asset and its volatility have the most impact.

What determines the option premium?

The option premium is determined by intrinsic and extrinsic value. The intrinsic value is the difference between the current price of the underlying asset and the strike price of the option. The extrinsic value takes into account the volatility of the underlying asset and the time left until the option expires.

What does theta tell you in options?

Theta tells you the rate at which the price of an option is expected to decline for each day that passes, assuming that all other factors remain constant. It’s also known as time decay. A high theta means that the option is losing value quickly as it approaches its expiration date.

Is negative theta good for options?

Negative theta isn’t good or bad. It simply means the option is losing value as time passes. For option buyers, negative theta is bad because it erodes the value of the option they bought. For option sellers, negative theta is good because the option they sold is decreasing in value, making it cheaper to buy back if they wish to close their position.

How does theta decay work in options trading?

Theta decay refers to the reduction in the value of an option as it approaches its expiration date. This is due to the decreasing likelihood that the option will end up in the money (profitable). Theta decay is not linear; it accelerates as the option gets closer to expiration.

Does theta decay on expiry day?

Yes, theta decay continues right up until the option expires. Theta decay accelerates as the option gets closer to its expiration date. This means the option loses value at an increasing rate as it nears expiration.