- October 24, 2020

- Posted by: CoachMike

- Categories: Options Trading, Trading Article

Options are the most flexible instruments in the world.

They are also the most misunderstood financial instruments.

The reason so many traders get frustrated using options is the lack of understanding of what impacts the price movement of an option. The terminology can be overwhelming for many newer traders

We always try to simplify things as much as possible for our traders at NetPicks. A great resource to use is our 2 Day Options Trading Crash Course.

It’s completely free of charge by clicking the links below.

Click Here for Options Trading Crash Course Day 1

Click Here for Options Trading Crash Course Day 2

We want to take one of the topics covered in Day 1 of the training to address a question that came up from one of our Nasdaq Options Superstars customers last week. The question that came up was, “What is an options delta and how do we use it to identify potential trade opportunities?”

What Is Delta In Options Trading?

Most people start trading options strictly by buying and selling individual calls and puts. While this is simple in theory, it can cause frustration at times when you get the stock to do exactly what you want it to and still not make money with the option contract that you chose to use.

This can happen when you don’t understand the different factors that impact the pricing of an option.

Definition of Delta

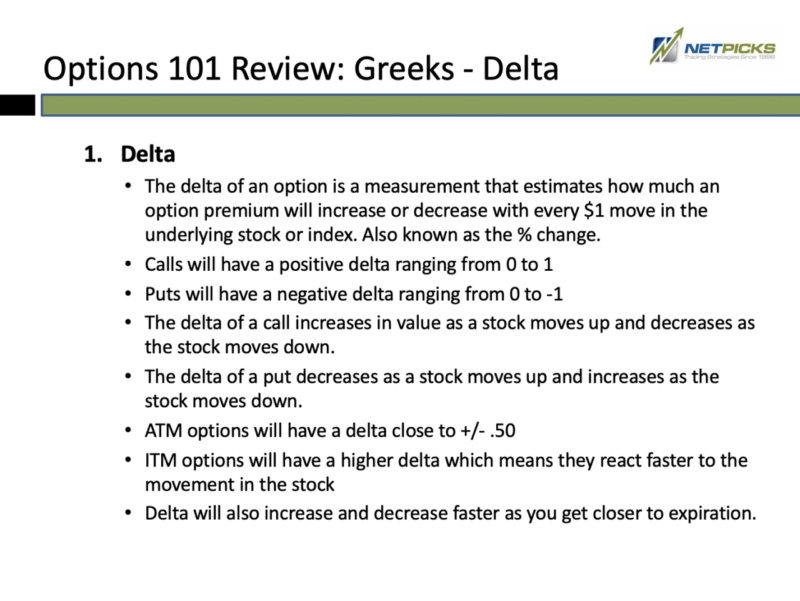

The delta of an option is a measurement that estimates how much an option will increase or decrease with every $1 move in the underlying stock or index. Also known as the % change.

For example, if buying an option that has a delta of .60 then that option will increase or decrease in value by $.60 for every $1 move in the stock price.

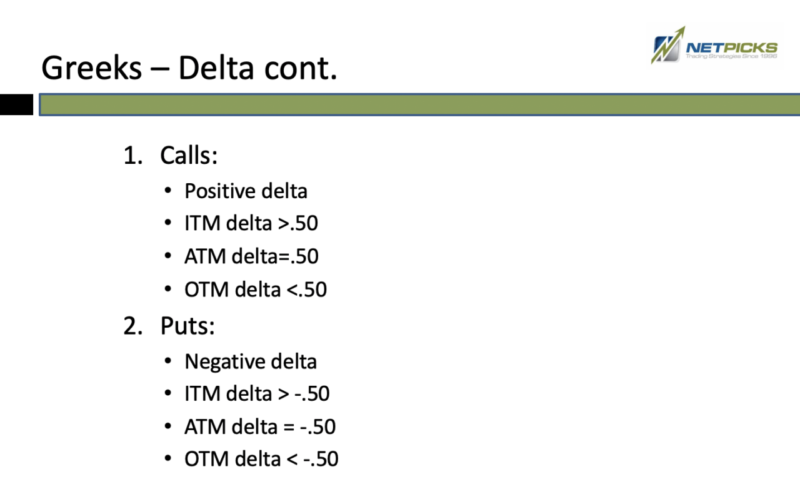

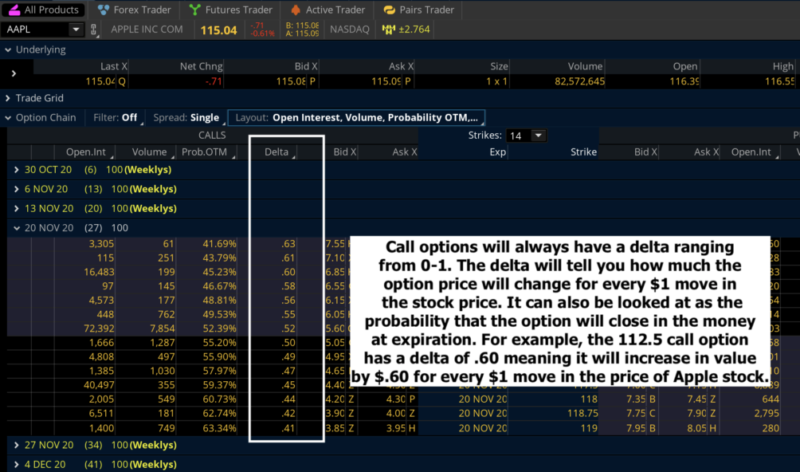

Call options will have a positive delta ranging from 0 to 1. The delta of a call option increases in value as a stock moves up and decreases as the stock moves down.

For example, let’s say you are looking to buy a call option as a bullish play on XYZ stock.

You buy the call option that has a delta of .60 meaning the option will increase in value by $.60 for every $1 move in the stock. After putting the position on, XYZ stock moves higher by $2 in your favor.

Now you look and see the delta is at .75. This means the option will continue increasing in value faster going forward on every subsequent $1 move higher in the stock value.

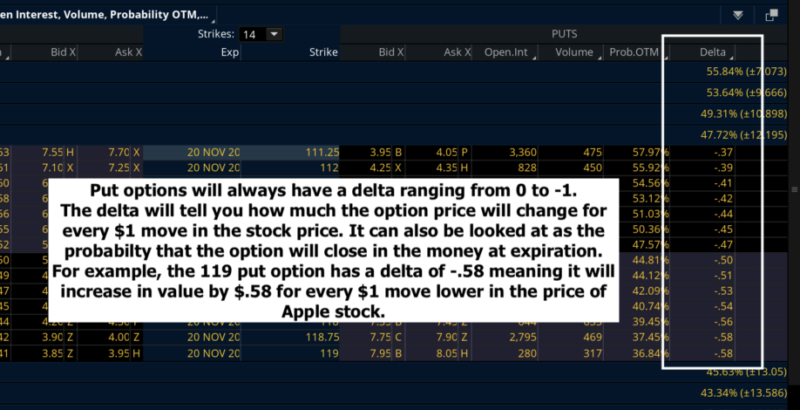

Put options will have a negative delta ranging from 0 to -1. The delta of a put option deceases in value as a stock moves up and increases as the stock moves down.

For example, let’s say you are looking to buy a put option as a bearish play on XYZ stock. You buy the put option that has a delta of .60 meaning the option will increase in value by $.60 for every $1 move in the stock. After putting the position on, XYZ stock moves lower by $2 in your favor. Now you look and see the delta is at .75. This means the option will continue increasing in value faster going forward on every subsequent $1 move lower in the stock value.

The delta of an option will also increase and decrease faster as you get closer to expiration. Options become more reactive to changes in stock price as you approach expiration. This can help produce a bigger profit potential if you get a quick move in your favor.

On the flipside, it can cause an issue when the stock moves against you as it will lead to larger losses. Short term options are higher risk and higher reward type trades.

At the money options will have a delta close to +/- .50. In the money options will have a higher delta meaning they will react faster to the movement in the stock.

The delta can also tell you the probability of that option closing in the money. If you are looking at a call option with a delta of .60, then that option has a 60% chance of closing in the money at expiration.

How do we use delta when buying options?

While many traders select the options that they are trading solely based on the price of an option, we like to take a different approach at NetPicks.

The trouble with buying a cheap out of the money option is the low probability of success that they give. Trading out of the money options is the most aggressive way to take an options trade.

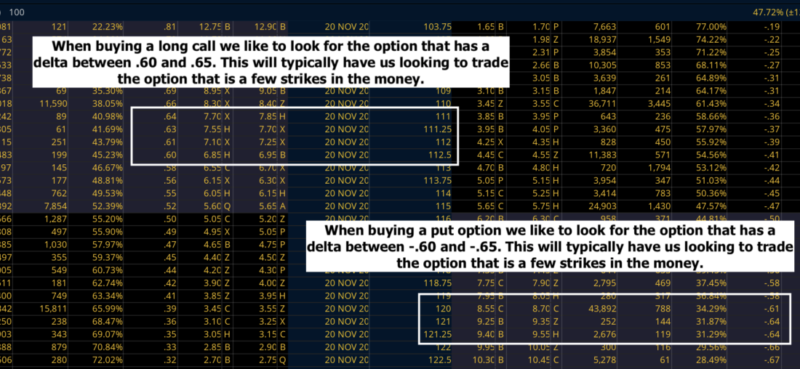

We prefer to use the options that will start to stack the odds in our favor. We can use the delta to help select the best strike price of the option that we are trading. When looking for a bullish trade, we like to use the call option with a delta between .60 and .65. This will typically have us trading an option that is a few strikes in the money.

If multiple strike prices have deltas inside of the .60-.65 range, then we will look to trade the option that has the highest volume and open interest. The better the liquidity, the easier it will be for us to trade those options.

When looking for a bearish trade, we like to use the put option with a delta between -.60 and -.65. This will typically have us trading an option that is a few strikes in the money.

If multiple strike prices have deltas inside of the -.60 and -.65 range, then we will look to trade the option that has the highest volume and open interest. The better the liquidity, the easier it will be for us to trade those options.

Trading the options with a delta inside of these ranges will give you the best bang for your buck. They will provide a quality position that will keep the cost at a reasonable level while also providing a great rate of return on a position that moves in your favor. They will also limit the time decay of the options.

How do we use delta when selling credit spreads?

One of our favorite trade types at NetPicks is selling credit spreads.

They are much more forgiving trades that lower the cost of the trades and also provide 5 ways of making money on the positions. We structure these trades initially by looking at the delta of the options.

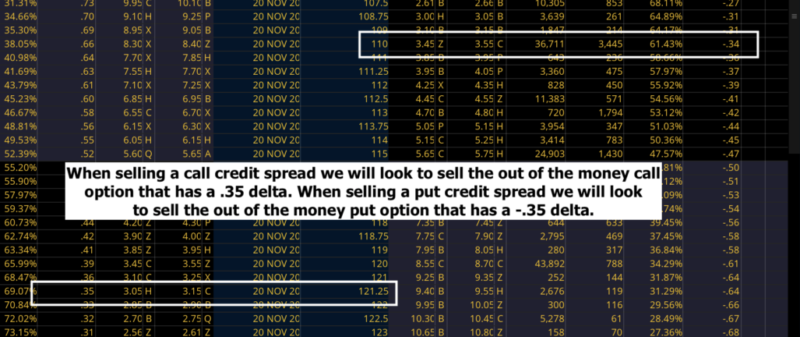

When selling a credit spread, we ideally like to sell the call or put option that has a delta as close to .35 as possible. By doing so we will be selling the option that has a 65% chance of closing out of the money. We want the options to get as cheap as possible so we can close them out at a cheaper price than what we sold them for when opening the trade.

We will then buy the option that is further out of the money and still allow us to collect between 30-40% of the width of the strikes.

For example, if we are selling the 135 call for $1.20 and buying the 137 call for $.40 that will allow us to sell the call credit spread for $.80 which is 40% of the width of the spread.

Looking for a delta of .35 on the option that we are selling will allow us to collect enough premium to give us a good risk to reward ratio.

We are typically looking to risk between 2 and 3 to make 1. We are ok with this ratio as the credit spreads give us 5 ways of making money on the trade and will give us a much higher probability of success.

Having defined criteria in place when trading options can help put the odds in your favor over time. While this criteria won’t guarantee a perfect 100% win rate, following these guidelines will help ensure the numbers will work in your favor as you build your sample set of trades larger.

Trading options is all a numbers game. If you can let the numbers dictate how you place and manage your trades, you will see far better growth in your account.

2 Comments

Comments are closed.

What about selling credit spread .35 delta and buying .10 delta. More risk but more return which is a decent probability. I understand that your safest bet is buying closer strike, but when 65% chance closing out of the money, it seems fair to buy the call with even lower delta. Perhaps, I’m thinking to sell credit spreads a day before expiration and after a run up and exhaustion and dying rsi

With a credit spread you need to balance the risk/reward. If you don’t collect enough premium up front you will have a risk/reward ratio that will be hard to work long term. We ideally want to be in a risk 2 or 3 to make 1 scenario.