- November 22, 2024

- Posted by: Shane Daly

- Category: Trading Article

If you’re getting into day trading, you’ll need to understand the complex tax implications that come with frequent market transactions. Your profits will face short-term capital gains rates, which can significantly impact your bottom line at tax time.

While you might find the prospect of paying up to 37% in taxes intimidating, there are legitimate strategies to minimize your tax burden and maximize your after-tax returns. From loss harvesting to qualifying for trader status, the U.S. tax code offers several opportunities to optimize your trading activities—if you know where to look.

TLDR

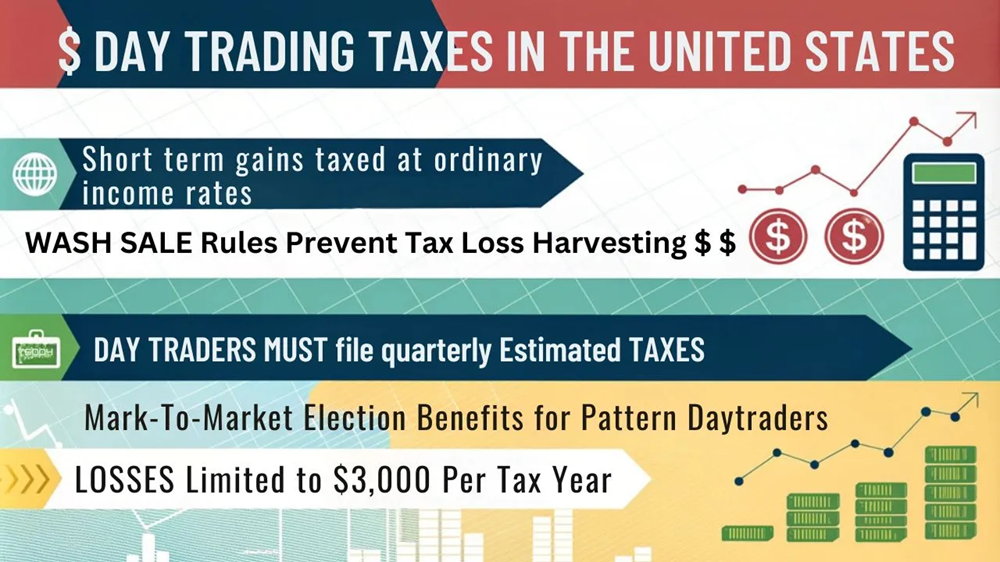

- Day trading profits are taxed as short-term capital gains at ordinary income rates ranging from 10% to 37%.

- Traders must prove substantial activity with four trading days per week and holding periods under 31 days.

- Capital losses can offset gains dollar-for-dollar, with a $3,000 annual limit against ordinary income.

- Qualifying traders can deduct business expenses like platform fees, market data subscriptions, and home office costs.

- Strategic tax planning includes loss harvesting, detailed record-keeping, and potentially using tax-advantaged accounts.

Understanding Day Trading Tax Rates

How do taxes affect your profits as a day trader? If you’re trading frequently, you’ll need to understand that your profits are typically taxed as short-term capital gains, which follow the same rates as your ordinary income. This means you could pay anywhere from 10% to 37% on your trading profits, depending on your total taxable income.

For example, if you’re a single filer making between $11,601 and $47,150 from all your income sources combined, you’ll pay 12% on your trading profits. As your income increases, so does your tax rate – jumping to 22% when you earn between $47,151 and $100,525. Day traders can use capital loss deductions up to $3,000 per year to offset their gains.

It’s important to note that these rates are significantly higher than long-term capital gains rates, which max out at 20%. Proper documentation of trades is VITAL since the IRS receives reports directly from brokers about your trading activities.

You’ll pay these higher short-term rates on any stocks or other securities you buy and sell within a year or less. This is why many day traders focus on tax planning strategies and carefully track their trades.

Understanding these tax brackets can help you better predict your after-tax profits and plan your trading strategy accordingly.

Offsetting Gains With Losses

A day trader’s best defense against high tax rates lies in strategic loss harvesting. You can offset your trading gains with losses to reduce your overall tax burden. When you sell investments at a loss, you can use these losses to cancel out your gains dollar for dollar, potentially saving significant money on taxes.

Trading platform fees can significantly impact your profits and tax situation.

Short-term gains from day trading are taxed at ordinary income rates. To make the most of loss harvesting, consider holding investments in tax-advantaged accounts like IRAs or 401(k)s, and always keep detailed records of your trades.

| Category | Tax Treatment |

|---|---|

| Short-Term Gains | Taxed as ordinary income (10-37%) |

| Long-Term Gains | Preferential rates (0%, 15%, 20%) |

| Income Thresholds | Based on filing status and total income |

| Loss Deductions | Up to $3,000 against ordinary income |

| Holding Period | Over 1 year for long-term treatment |

There’s a key limit you should know about: if your losses exceed your gains, you can only deduct up to $3,000 against your ordinary income in any given year. Don’t worry about losing the excess, though – you can carry these losses forward to future tax years. For married couples filing separately, this limit drops to $1,500 each.

Watch out for the wash sale rule when you’re offsetting gains. If you sell a security at a loss and buy it back within 30 days, you can’t use that loss for tax purposes.

It’s smart to set aside money for taxes and consider making estimated tax payments to avoid penalties.

Qualifying As A Trader

Qualifying as a trader in the eyes of the IRS requires meeting strict criteria that separate you from casual investors. You’ll need to demonstrate substantial and regular trading activity by executing trades on most market days – typically around four days per week.

Your average holding period should be 31 days or less, as the focus is on profiting from short-term market movements. A minimum deposit of $25,000 is required with your broker if you plan to be a pattern day trader.

To be considered a trader, you must treat your trading as a genuine business venture. This means dedicating significant time – at least 16 hours weekly – to market analysis, research, and trading activities. It’s recommended to execute at least 720 trades annually to meet IRS requirements.

You’ll need a proper setup, including necessary equipment and a dedicated workspace, along with ongoing education to improve your trading skills.

| Expense Category | What Qualifies | Maximum Deduction |

|---|---|---|

| Business Equipment | Computers, monitors, software | Full cost or depreciation |

| Educational Costs | Trading courses, seminars | 100% of qualified expenses |

| Home Office | Dedicated trading space | Percentage of home expenses |

| Travel Expenses | Trading conferences, meetings | Actual costs plus per diem |

| Professional Fees | Tax advisors, consultants | Full amount of fees |

Keeping detailed records is key. You’ll need to maintain separate accounts for trading and investment activities, and properly document all your transactions.

You should report your business expenses on Schedule C and use Form 4797 if you’ve made a mark-to-market election.

Essential Tax Deductions

Successful day traders can significantly reduce their tax burden by properly claiming essential deductions. You’ll need to ensure your expenses meet the IRS criteria of being both common and helpful for your trading business.

Keep detailed records of all your trading-related expenses, as they’ll be important during tax filing.

Professional traders who meet specific requirements can elect mark-to-market accounting to avoid capital loss limitations.

Here are the key deductions you can claim as a day trader:

- Trading platform subscriptions and software costs

- Research tools and market data fees

- Home office expenses related to your trading activities

- Educational materials and professional development costs

Remember that you can offset your capital gains with losses, and if your losses exceed your gains, you’re allowed to deduct up to $3,000 against your ordinary income.

Any remaining losses can be carried forward to future tax years. Be careful with the wash sale rule – if you buy substantially similar securities within 30 days of selling at a loss, you can’t claim that loss immediately.

Consider using tax-advantaged accounts like IRAs or 401(k)s to defer taxes on your trading profits and manage your tax liability more effectively.

Smart Tax Planning Methods

Smart tax planning starts well before the tax filing deadline and requires a strategic approach throughout the year.

You’ll need to keep detailed records of all your trades and set aside money for taxes as you earn profits. This helps you avoid surprises when it’s time to file your returns.

To minimize your tax burden, you can consider holding profitable positions for more than a year to qualify for lower long-term capital gains rates.

If you’re trading frequently, you might want to look into qualifying as a “trader in securities,” which lets you deduct business expenses and potentially benefit from the Qualified Business Income deduction.

You should also think about using tax-advantaged accounts like IRAs or 401(k)s for some of your trading activities. These accounts can help defer taxes until retirement.

At year-end, you can use strategies like harvesting losses to offset gains or timing your trades to push gains into the next tax year.

Your Questions Answered

How Do International Tax Treaties Affect US Day Traders Trading Foreign Stocks?

When you trade foreign stocks, tax treaties protect you from paying taxes twice on the same income.

You’ll need to report your worldwide trading income to the IRS, but these agreements let you claim foreign tax credits through Form 1116.

This means if you’ve paid taxes on trading profits in another country, you can reduce your US tax bill by that amount.

Can Day Trading Profits Impact Eligibility for Government Benefits or Financial Aid?

Your day trading profits can significantly impact your eligibility for government benefits and financial aid.

Since trading income counts toward your adjusted gross income, you’ll need to report it.

This can affect your access to Medicaid, SNAP benefits, housing assistance, and federal student aid.

Higher profits may reduce or eliminate your eligibility for these programs, as most use income-based thresholds for qualification.

What Are the Tax Implications of Using Margin Accounts for Day Trading?

When you trade using margin accounts, your profits are taxed as ordinary income for trades held less than a year.

You can deduct margin interest, brokerage fees, and regulatory costs from your taxable income.

Keep in mind that trading profits might push you into a higher tax bracket.

You’re limited to $3,000 in capital loss deductions against ordinary income, but excess losses can carry forward to future years.

How Does Cryptocurrency Day Trading Differ From Stock Trading for Tax Purposes?

When you’re day trading crypto, you’ll notice key tax differences from stocks.

There’s no wash sale rule for crypto, meaning you can sell at a loss and rebuy immediately for tax benefits.

Crypto trades are taxed as property sales, and you’ll need to track every transaction carefully.

Mining and staking earnings are taxed as regular income, unlike stock dividends which often get preferential treatment.

Do State-Specific Tax Regulations Affect Day Trading Differently Across Various States?

Yes, your day trading experience will vary significantly based on your state’s tax regulations.

You’ll face higher tax rates in states like California and New York compared to Florida and Texas, which have no state income tax.

Your state’s rules also affect available deductions, business expense claims, and filing requirements.

Consider these differences when planning your trading strategy and choosing where to live.

Disclaimer: I am not a tax professional or tax lawyer. The information provided here is for general informational purposes only and should not be considered as professional tax advice. For specific tax-related questions or issues, please consult with a qualified tax professional or legal advisor to ensure that you receive accurate and personalized guidance tailored to your individual circumstances.