- March 2, 2026

- Posted by: Shane Daly

- Categories: Day Trading, Trading Article

You’d expect that quitting your day job to trade full-time would improve your performance—after all, you’ve got complete focus, unlimited hours to analyze setups, and zero distractions from meetings or commutes. The reality, however, moves in the opposite direction for most traders; win rates decline, drawdowns deepen, and psychological strain intensifies within the first three to six months of going full-time. The issue isn’t lack of skill—it’s a fundamental shift in how pressure, time, and identity converge to sabotage your decision-making process.

The Executive Summary

- Removing time constraints from part-time trading increases decision fatigue and leads to overtrading marginal setups instead of selective high-conviction trades.

- Financial pressure transforms trading from using discretionary income to survival dependency, amplifying loss aversion and eroding emotional resilience.

- Excessive screen time creates boredom that masquerades as opportunity, causing traders to justify mediocre setups they would normally avoid.

- Loss of external employment structure removes disciplined routines, deteriorating execution quality without deliberate self-imposed frameworks and rituals.

- Insufficient capital buffers force premature profit-taking and oversized positions, violating sound risk management due to immediate financial needs.

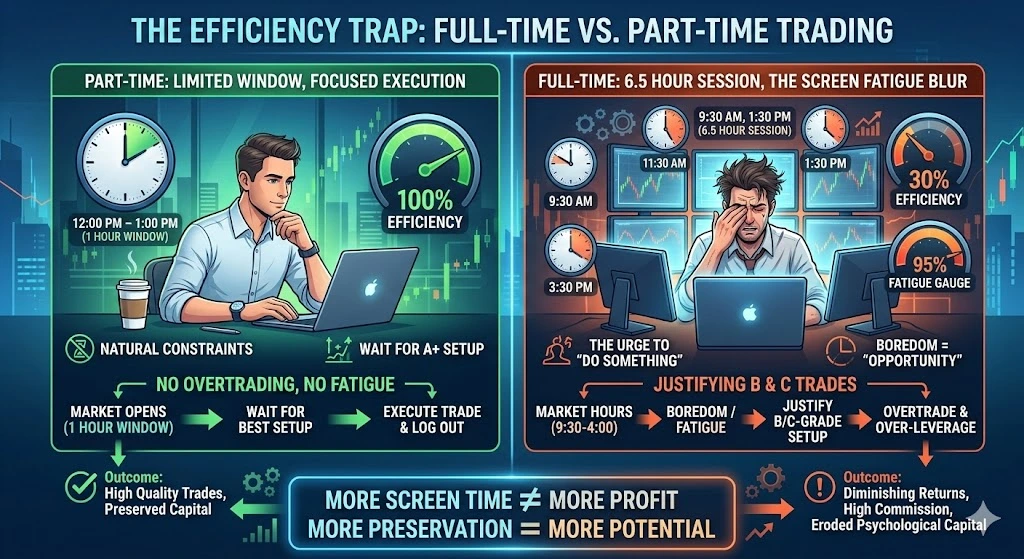

The Paradox of More Time, Worse Results

When traders shift from part-time to full-time participation in the markets, they often experience a counterintuitive decline in performance—not because they lack skill or dedication, but because the structural constraints that previously governed their behavior have been removed.

Part-time trading enforces selective trading through natural time management limitations; you’re forced to identify only high-conviction setups that meet strict criteria, promoting quality over quantity in your execution.

Full-time availability, however, introduces decision fatigue—you’ll overthink entries, babysit positions unnecessarily, and exit prematurely due to constant market exposure.

The scarcity that once enhanced focus and maintained emotional detachment disappears; abundance eliminates the filter that protected you from marginal trades, degrading overall performance through increased activity rather than improved results.

The Psychological Shift from “Want” to “Need”

The shift from discretionary income to survival dependency fundamentally alters your risk perception framework, creating what behavioral finance researchers identify as loss aversion asymmetry—where the psychological impact of losing $1,000 exceeds the satisfaction of gaining the same amount by a factor of approximately 2.5 to 1.

| Action | Optional Income (Want) | Survival Dependency (Need) |

|---|---|---|

| Profits | Follows system targets. | Prematurely closed to “lock in” cash. |

| Losses | Mechanical stop-loss execution. | Avoided/Held to prevent failure. |

| Psychology | Probabilistic / Neutral. | Loss Aversion / Survival Instinct. |

When your mortgage depends on monthly P&L, financial pressure erodes the emotional resilience required for systematic trading; you’re watching positions through a distorted lens where every drawdown threatens basic security rather than representing acceptable variance within your statistical edge.

This psychological transformation degrades your trader mindset—causing premature profit-taking to secure “guaranteed” income and extended loss-holding to avoid realizing failures—effectively inverting ideal position management.

Your risk tolerance contracts precisely when maintaining discipline matters most, as survival instincts override the probabilistic thinking that generated success when trading remained optional.

Overtrading and the Screen Time Trap

Beyond the psychological pressure that survival dependency creates, full-time trading introduces a structural problem that part-time traders naturally avoid—the perception that market hours represent work hours requiring productivity.

When you’re watching screens from 9:30 to 4:00, boredom disguises itself as opportunity, and screen fatigue convinces you that mediocre setups deserve execution. You start justifying B and C grade trades because idle capital feels like opportunity cost, even though quality setups don’t increase proportionally with observation time.

Part-time traders face natural constraints; they can’t overtrade during limited windows. Full-time traders, however, must actively resist the impulse to “do something” when markets offer nothing compelling.

The most profitable professionals trade less frequently than struggling full-timers—they wait for A+ setups and ignore everything else, understanding that preservation trumps participation.

Loss of Structure and Routine

Full-time trading strips away the external scaffolding that employment provides—designated start times, mandatory meetings, lunch breaks, commute rituals—leaving you entirely responsible for imposing order on your days.

Without deliberate structured routines, trading discipline deteriorates rapidly; you’re sleeping until markets open, skipping exercise, reviewing charts until midnight without clear boundaries separating work from personal life.

Effective time management requires establishing non-negotiable daily rituals: market preparation at 8:00 AM, trading sessions ending at 3:00 PM, mandatory review periods, scheduled breaks.

These personal boundaries aren’t optional—they’re foundational to emotional regulation, preventing the psychological drift that transforms disciplined analysis into reactive gambling.

The traders who maintain performance after going full-time treat their schedules with the same dedication they apply to risk management, understanding that structural consistency directly correlates with execution quality.

Identity and Self-Worth Get Tied to P&L

Identity fusion with your profit-and-loss statement represents one of trading’s most insidious psychological traps, particularly acute when professional alternatives disappear and market performance becomes your sole measure of competence.

| Mental Metric | Fused Identity (P&L Trap) | Resilient Identity (Decoupled) |

|---|---|---|

| Market Loss ($-$$$) | A direct attack on competence/intelligence. | A statistical inevitability within an edge. |

| Mental Focus | Obsession with “today’s performance.” | Execution quality and process. |

| Core Emotion | Existential Doubt. | Probabilistic Confidence. |

| Drawdown Survival | Triggers identity crises and “revenge trading.” | Creates a period of review; not doubt. |

When you’re watching your account balance define your self-worth, every drawdown triggers a self-identity crisis—transforming temporary underperformance into existential doubt about your capabilities, intelligence, and value as a professional.

This psychological coupling destroys the emotional detachment necessary for objective decision-making; instead of viewing losses as statistical inevitabilities within your edge, you interpret them as personal failings.

The solution requires deliberately constructing identity outside trading—whether through relationships, physical pursuits, or intellectual interests—that provide validation independent of daily returns, creating psychological resilience when markets inevitably move against your positions and preventing the catastrophic thinking that fuels revenge trading.

The Capital and Runway Mistake

While psychological pitfalls undermine trading performance from within, most full-time traders fail for a much simpler reason—they’re mathematically undercapitalized from day one, creating financial pressure that forces suboptimal decisions regardless of their emotional discipline or market knowledge.

The capital allocation error manifests in three distinct ways:

- Insufficient financial buffer: You’re watching your account balance while simultaneously calculating rent, knowing you have 4-6 months maximum before forced liquidation.

- Premature profit withdrawal: You pull winning trades early because groceries can’t wait, destroying your risk management framework and position sizing ratios.

- Oversized positions: You leverage beyond your trading psychology tolerance—risking 5-8% per trade instead of your planned 1-2%—because monthly expenses demand immediate returns.

Smart shifts require twelve to twenty-four months of living expenses separated entirely from trading capital.

How to Transition Successfully

Because most traders conceptualize the change to full-time status as a single decision—employed today, self-employed tomorrow—they skip the developmental architecture that separates sustainable careers from expensive failures.

You’re watching opportunity costs compound when you haven’t formalized your trading plan, strengthened emotional resilience through simulated full-day sessions, or conducted market research that validates edge persistence across market regimes.

Treat the shift like launching a business—maintain emergency savings untouched, preserve part-time income during overlap periods, and implement strict trading hours with end-of-day cutoffs that prevent overtrading.

Your risk management protocols need recalibration for drawdown scenarios that threaten living expenses, not discretionary capital.

Continue journaling and reviewing trades; going full-time isn’t graduation but rather a new operational framework requiring more discipline, not less, while preserving hobbies and relationships outside markets.

The Knowledge Gap

Should I Keep My Day Job While Building My Trading Account Size?

Yes, you should maintain your day job while building account size—this approach preserves financial security, which directly supports emotional stability and trading discipline.

When you’re not dependent on trading profits for living expenses, you’ll execute superior risk management decisions without psychological pressure to overtake positions or abandon your strategy.

Full-time trading before achieving sufficient capital often compromises decision-making; maintaining employment provides the stability necessary for disciplined, methodical account growth without emotional interference from financial desperation.

How Much Savings Do I Need Before Going Full-Time as a Trader?

You’ll need at least 12-24 months of living expenses as a financial cushion before moving to full-time; this buffer protects your trading psychology from performance pressure when income becomes irregular.

Calculate your monthly expenses—rent, utilities, insurance, food—then multiply by 18 months minimum.

Without this safety net, you’re likely to overtrade, chase losses, or abandon solid strategies prematurely, since desperation compromises decision-making and forces you to prioritize immediate profits over long-term consistency.

Can Part-Time Traders Actually Outperform Full-Time Professional Traders?

Yes, part-time performance can exceed full-time traders’ results because you’re maintaining emotional discipline—you won’t overtrade during low-probability setups.

Your limited time commitment forces superior risk management; you’ll focus on high-quality trading strategies rather than forcing positions to justify full-time status.

Part-timers often handle market volatility better since their livelihood doesn’t depend entirely on each trade, reducing the psychological pressure that degrades decision-making when you’re watching every tick movement.

What Are the Tax Implications of Switching to Full-Time Trading Income?

You’ll face significant changes in your tax bracket since full-time trading income—whether from capital gains or ordinary income—requires thorough income reporting throughout the year.

You’re watching your trading deductions expand to include home office expenses, data subscriptions, and equipment; however, you’ll need meticulous expense tracking to substantiate these claims.

Shifting also affects retirement accounts, as self-employment income enables SEP-IRA or Solo 401(k) contributions that weren’t available with part-time status.

Do Professional Traders Recommend Starting With Prop Firms or Personal Capital?

You’ll find most professional traders recommend starting with prop firms rather than personal capital—they provide structured risk management frameworks, defined capital allocation limits, and objective performance metrics that accelerate your trading experience.

Prop firms eliminate the psychological pressure of risking your own money while you’re developing consistent profitability; meanwhile, trading personal capital too early often leads to undercapitalized positions, emotional decision-making, and account depletion before you’ve established proper edge verification through statistically significant sample sizes.

Next Move

Going full-time doesn’t guarantee better performance—it often degrades it through psychological pressure, structural deficits, and capital mismanagement. You’ll need deliberate systems to counteract these forces: maintain rigid routines regardless of market hours, separate identity from P&L fluctuations, and make certain your runway extends beyond twelve months to buffer emotional decision-making. The shift succeeds when you’re treating trading as disciplined business operations, not chasing freedom or validation through increased screen time and position frequency.