- February 26, 2026

- Posted by: Shane Daly

- Category: Trading Article

You’ve probably thought about quitting your day job to trade full-time, waking up without an alarm, and finally focusing on what could make you real money. But here’s what most traders won’t tell you: quitting too early doesn’t just risk your savings—it fundamentally changes how you’ll trade. Before you submit that resignation letter, there’s a specific financial threshold you’ll need to hit, and it’s likely higher than you think.

The Executive Summary

- Validate your trading system with at least 12-24 months of consistent, documented live performance across different market conditions.

- Calculate required capital by dividing annual income needs by conservative expected returns, accounting for taxes and drawdowns.

- Maintain a separate 12-month cash reserve for living expenses to avoid forced withdrawals during losing periods.

- Keep your job during the transition to provide financial stability and reduce pressure to generate trading income.

- Ensure mathematical justification exists for the career shift; inspirational returns alone don’t warrant quitting employment.

Calculate Your Capital Requirement for Full-Time Trading

How much money do you actually need before you can trade for a living? The capital calculation starts with a fundamental equation: divide your annual income target by your expected annual return.

If you need $50,000 yearly and project a 20% return, you’ll require $250,000 in trading capital. However, you must adjust for taxes, fees, and sequence risk—yearly returns fluctuate considerably.

| Annual Income Target | Monthly Target | 10% Return | 15% Return | 20% Return | 25% Return | 30% Return |

|---|---|---|---|---|---|---|

| $30,000 | $2,500 | $300,000 | $200,000 | $150,000 | $120,000 | $100,000 |

| $50,000 | $4,167 | $500,000 | $333,333 | $250,000 | $200,000 | $166,667 |

| $100,000 | $8,333 | $1,000,000 | $666,667 | $500,000 | $400,000 | $333,333 |

| $150,000 | $12,500 | $1,500,000 | $1,000,000 | $750,000 | $600,000 | $500,000 |

Note: These figures represent gross capital requirements. To account for taxes (approx. 20-30%) and a safety buffer for drawdowns, it is recommended to have 25-50% more capital than the amounts listed above.

Your income strategy should include a separate cash reserve of at least twelve months’ living expenses outside your trading account. This buffer prevents forced withdrawals during drawdowns and reduces emotional volatility that degrades your trading execution under financial stress.

Don’t rely on aspirational return percentages. Use validated, historically-proven performance data across different market regimes to set realistic expectations.

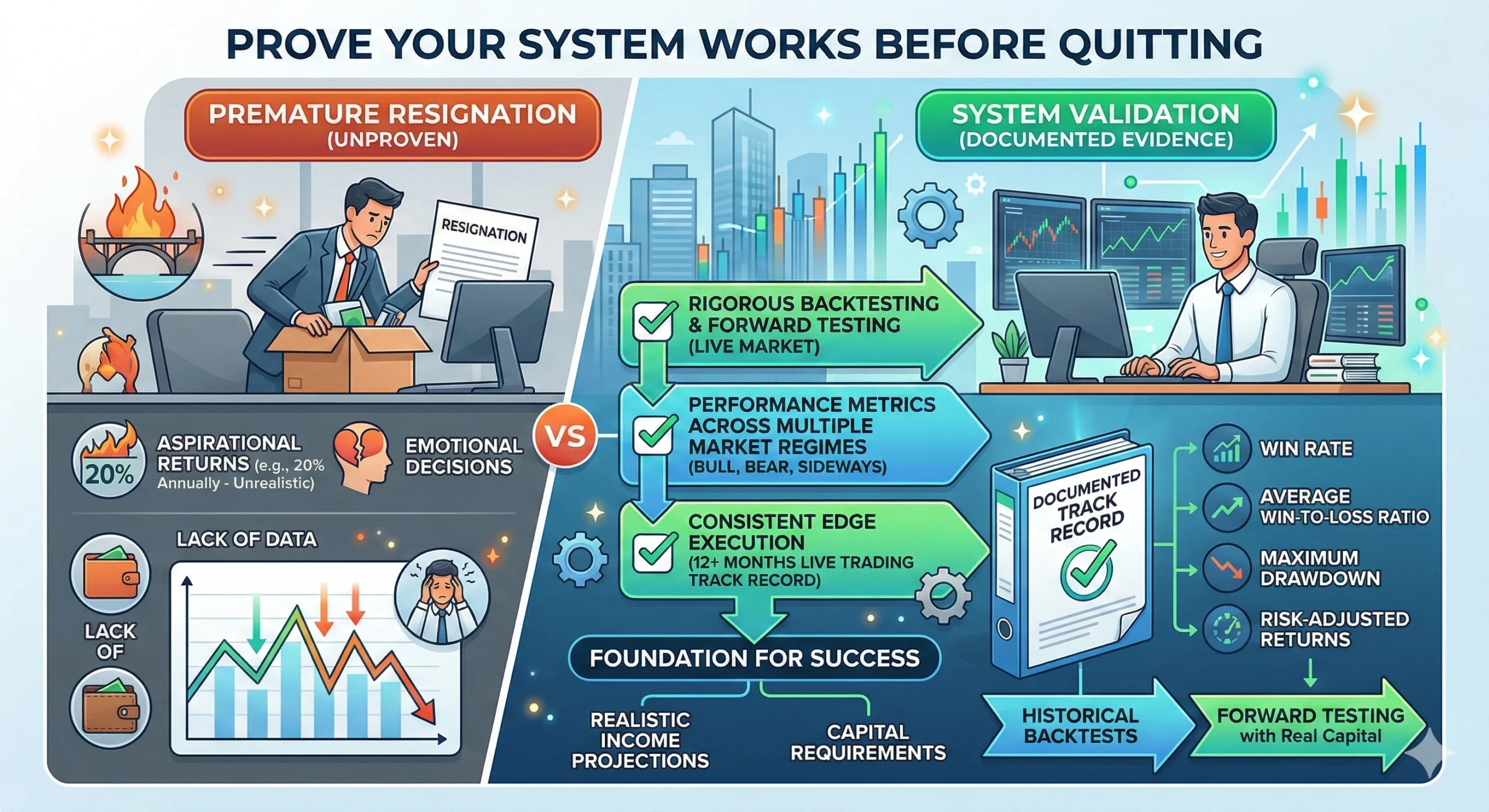

Prove Your System Works Before Quitting

Before you resign from your job, you must validate your trading system through rigorous backtesting and forward testing in live market conditions.

System validation requires examining performance metrics across multiple market regimes—bull markets, bear markets, and sideways consolidations. You’ll need documented evidence showing consistent edge execution over at least 12 months of live trading.

Track your win rate, average win-to-loss ratio, maximum drawdown, and risk-adjusted returns. These performance metrics reveal whether your system generates sustainable income or simply benefited from favorable market conditions.

Historical backtests provide initial confidence, but forward testing with real capital confirms your ability to execute under actual trading stress.

Don’t rely on aspirational returns like 20% annually until you’ve proven them consistently. Your documented track record becomes the foundation for realistic income projections and capital requirements.

Build Your 12-Month Safety Net

Once you’ve validated your trading system, you must establish a cash reserve equal to twelve months of living expenses—completely separate from your trading capital. This emergency fund prevents forced withdrawals during drawdowns, which would otherwise compound losses and damage your account’s compounding potential.

| Scenario | Housing | Food | Transport | Insurance | Utilities | Total/Month | 12-Month Net |

|---|---|---|---|---|---|---|---|

| Conservative | $1,200 | $400 | $300 | $250 | $150 | $2,900 | $34,800 |

| Moderate | $2,000 | $600 | $450 | $400 | $250 | $4,800 | $57,600 |

| High | $3,500 | $900 | $700 | $600 | $400 | $8,100 | $97,200 |

Safety net strategies include maintaining liquid assets in high-yield savings accounts or money market funds—never in your brokerage account where emotional access becomes problematic.

Calculate your actual monthly expenses: housing, utilities, food, insurance, and discretionary spending. Multiply by twelve. This figure represents your minimum cushion before moving to full-time trading.

Without this buffer, financial pressure forces suboptimal trading decisions: cutting winners prematurely, averaging down on losses, or forcing trades to generate income.

Your emergency fund isn’t optional—it’s the foundation that allows disciplined execution under real-world conditions.

Why Withdrawals Kill Compounding

When you withdraw trading profits to cover living expenses, you’re not just removing cash—you’re eliminating future returns that cash would’ve generated. The compounding effects matter greatly over time.

| Scenario | Starting Capital | Annual Return | Years | Ending (No Withdrawals) | Ending (With $50k/yr Draw) |

|---|---|---|---|---|---|

| Long-Term Growth | $250,000 | 20% | 10 | $1,547,934 | $579,144 |

Consider these withdrawal strategies impacts:

- $250,000 compounded at 20% for 10 years: Grows to approximately $1.5 million with zero withdrawals.

- Same account with $50,000 annual withdrawals: Ends at roughly $580,000—a $920,000 difference.

- Each dollar withdrawn eliminates its exponential growth potential across all future periods.

- Regular withdrawals force you into “income mode” rather than “growth mode.”

- Tax implications compound the damage: You’re paying taxes on withdrawn gains that could’ve remained invested.

Data-driven traders separate their runway from trading capital. This approach maximizes compounding effects while maintaining regulatory-compliant risk management.

How Trading Pressure Breaks Your Execution

Financial pressure transforms disciplined traders into emotional decision-makers. When you’re dependent on trading income, each position carries psychological weight beyond its market risk.

Trading psychology research demonstrates that financial stress compromises execution quality—you’ll cut winning trades early to lock in grocery money, or hold losing positions hoping they’ll recover to cover bills.

Your emotional resilience deteriorates under sustained income pressure. You’ll recognize setups don’t match perfectly but take trades anyway because you need the income.

This behavior pattern consistently degrades edge quality. Data shows traders performing worse after shifting to full-time trading due to increased pressure, not decreased skill.

The solution isn’t willpower—it’s structural. Maintain stable income sources until your trading capital generates sustainable returns without emotional interference from living expenses.

Are You Actually Ready to Go Full-Time?

Most traders misjudge their readiness because they conflate trading profitably with trading professionally. Your trading psychology changes dramatically when market performance determines whether you pay rent.

Before quitting your day job (main source of income), verify you meet these criteria:

- Capital adequacy: Your account can generate required income at conservative return rates (10-15%, not aspirational 30%).

- Cash runway: Minimum twelve months of living expenses outside your trading account.

- System validation: Backtested and forward-tested results across multiple market regimes.

- Income stability: Consistent monthly returns for at least 18-24 months in live conditions.

- Execution consistency: Documented adherence to trading rules without emotional deviations.

If any criterion isn’t met, keep your job. The pressure of forced withdrawals during drawdowns will compromise your edge when you need it most.

The Case for Trading Part-Time First

Before risking your career, part-time trading offers a validation path that preserves income stability while you refine your edge.

You’ll maintain consistent income while testing your system across different market conditions, building the track record necessary for objective assessment. This approach strengthens emotional resilience since you’re not dependent on trading profits for living expenses, eliminating the pressure that degrades execution quality.

Part-time trading reveals critical gaps in your risk management framework before they threaten your financial security.

You’ll identify weaknesses in position sizing, stop-loss discipline, and drawdown recovery while your job provides a safety net. Track execution consistency, rule adherence, and actual returns versus projections.

Only when your documented performance proves sustainable across multiple quarters should you consider moving to full-time.

Does Your Plan Justify Leaving Your Job?

Why would you abandon steady income without quantifiable proof your trading plan generates superior risk-adjusted returns? Your decision requires rigorous financial validation before emotional commitment overrides rational analysis.

Evaluate these critical benchmarks:

- Capital adequacy: Required capital equals annual income target divided by validated annual return percentage.

- Cash runway: Maintain twelve months of living expenses separate from trading capital.

- System validation: Documented backtesting and forward testing across multiple market regimes.

- Emotional resilience: Proven ability to execute consistently during drawdown periods exceeding thirty percent.

- Trading mindset: Evidence of rule adherence without income pressure distorting decision-making.

Your numbers must align before resignation. Aspirational returns don’t pay bills—verified performance does. If your current results can’t justify the shift mathematically, maintain employment while refining your edge.

The Knowledge Gap

What Health Insurance Options Exist for Full-Time Traders Without Employer Coverage?

You’ll need self-employment insurance through the ACA marketplace, private insurers, or professional trader associations.

Compare plans carefully—premiums, deductibles, and network coverage vary considerably.

Consider high-deductible plans paired with Health Savings Accounts for tax advantages and lower premiums.

Factor insurance costs into your capital requirements; they’re non-negotiable expenses that increase your minimum income needs.

Don’t overlook COBRA as a temporary bridge, though it’s typically expensive.

Review options annually during open enrollment.

How Do I Handle Retirement Contributions When Trading Full-Time Versus Employed?

You’ll need to establish a solo 401(k) or SEP-IRA as a self-employed trader, though contribution limits depend on your documented trading income structure.

Traditional employment offers automatic retirement contributions and potential employer matching—benefits you’ll lose.

Consider tax implications carefully: retirement accounts provide tax-deferred growth, but full-time trading income fluctuates unpredictably.

Maintain detailed records for regulatory compliance and consult a tax professional to optimize your retirement strategy based on consistent, verified trading performance data.

Can I Return to Corporate Work if Full-Time Trading Fails?

You can return, but it’s not guaranteed. The job market changes rapidly, and employment gaps raise red flags for recruiters.

Your industry connections weaken over time, and skill relevance diminishes as technology and practices evolve. Financial stability suffers during change periods.

Before quitting, you should maintain professional networks, document transferable skills, and make certain you’ve got substantial runway capital.

Re-entry becomes progressively harder the longer you’re away from corporate environments.

Should I Tell Others I’m Quitting to Trade Full-Time?

You shouldn’t announce your career change until you’ve validated your trading system, secured twelve months of living expenses, and proven emotional readiness through consistent performance.

Sharing prematurely adds social pressure that can compromise your trading mindset and force suboptimal decisions to meet others’ expectations.

Protect your personal finances by keeping plans private until your data confirms sustainable returns.

If you must share, discuss it only after you’ve already achieved documented success and financial stability.

How Does Full-Time Trading Affect Mortgage Applications and Credit Eligibility?

Full-time trading complicates mortgage applications because lenders prioritize income stability, typically requiring two years of consistent self-employment documentation.

Your credit score remains unaffected by employment status, but reduced verifiable income and irregular cash flows raise lender concerns.

You’ll need thorough tax returns, bank statements, and profit-loss records. Many lenders view trading income skeptically compared to W-2 employment.

Maintain detailed financial records and consider applying before shifting to strengthen your qualification position.